Introducing Index Advantage+ Select Income™ Annuity, a new registered index-linked annuity (RILA) that builds on a decade of innovation to offer enhanced flexibility and income strategies as dynamic as your clients’ goals.

Experience the freedom of a RILA reimagined

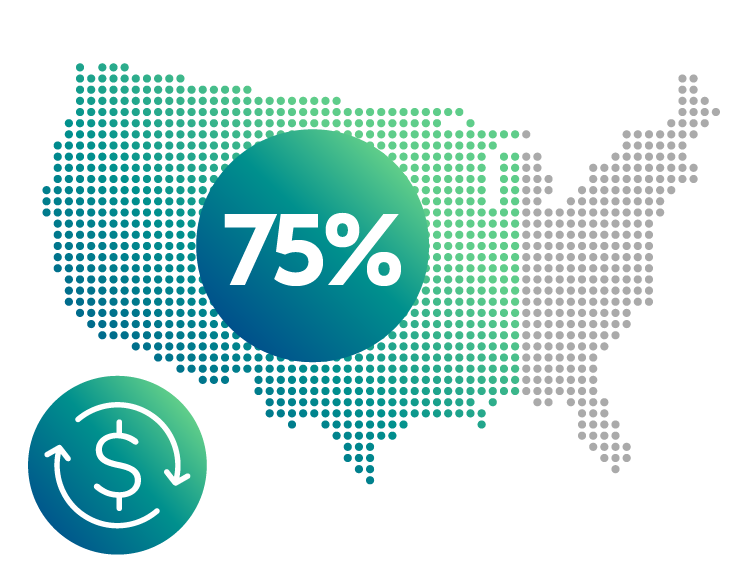

Americans seek flexible retirement products to boost income potential

In fact, 75% are interested in a retirement product that allows them to adjust their investment risk after they begin receiving income, with the goal of potentially increasing their retirement income.1

[Narrator] Introducing our new Index Advantage+ Select Income™ Annuity. Experience the freedom to select when clients start lifetime income and which strategies best match your clients’ needs. Building on a decade of innovation, it reimagines the income registered index-linked annuity, or RILA, experience, offering enhanced flexibility and income strategies as dynamic as your clients’ goals.

[On-screen disclosure] Income provided by the Income Benefit rider. The rider fee is 0.70% accrued daily and deducted on each quarterly contract anniversary, calculated as a percentage of the charge base, which is the contract value on the preceding quarterly contract anniversary, adjusted for subsequent purchase payments and withdrawals. The Income Benefit is automatically included in the contract at issue and cannot be added to a contract after issue. [End of on-screen disclosure]

Your clients can now choose to start their lifetime income stream when it makes sense for them.

[On-screen disclosure] Once you reach age 50 and have satisfied the 1-index-year income payment waiting period, Lifetime Income Payments can begin any time up to 14 calendar days before and Index Anniversary. [End of on-screen disclosure]

At income election, clients can choose from Level or Dynamic income options, and then find a strategy that matches their risk tolerance and financial goals, whether that's aggressive, conservative, or somewhere in between.

[On-screen disclosure] Both 1-year term and multi-year term index options are available during accumulation, prior to electing income payments. 1-year term index options are available on both Level and Dynamic Income options. [End of on-screen disclosure]

Index Advantage+ Select Income™ is designed to deliver outcomes that help meet your clients' needs and can adapt as their life changes. Find out if our reimagined solution is right for your clients. Call our Sales Desk for more information or speak directly with your Allianz® representative today.

[On-screen disclosures]

For more complete information about Index Advantage+ Select Income™ and the variable option(s), call Allianz Life Financial Services, LLC at 800.542.5427 for a prospectus. The prospectuses contain details on investment objectives, risks, fees, and expenses, as well as Other information about the RILA and the variable option(s), which your clients should carefully consider. Encourage your clients to read the prospectuses thoroughly before sending money.

Lifetime income assumes all terms of the contract are followed and no more than the annual maximum income payment is token. Excess withdrawals reduce the contract value, income payments, and any guaranteed death benefit value, and may end the contract.

Registered index-linked annuities (RILAs) provide indexed return potential with the opportunity for varying levels of protection through multiple index options available prior to receiving annuity payments, tax-deferred gro%'fr potential, a variety of annuity options, and a death benefit during the accumulation phase.

RILAs are subject to investment risk, including possible loss of principal. Investment returns and principal value will fluctuate with market conditions so that contract value, upon distribution may be worth more or less than the original cost.

Withdrawals will reduce contract values (including any cash value) and the value of any potential protection benefits.

Withdrawals taken within the period stated in the prospectus will be subject to a withdrawal charge or a market value adjustment (MVA), depending on the product.

All withdrawals are subject to ordinary income tox and if taken prior to age 59½, may be subject to a federal additional tax.

Guarantees are backed solely by the financial strength and claims-paying ability of the issuing insurance company and do not apply to the performance of the variable subaccount(s), which will fluctuate with market conditions.

• Not FDIC insured • May lose value • No bank or credit union guarantee • Not a deposit • Not insured by any federal government agency or NCUA/NCUSIF

Products are issued by Allianz Life Insurance Company of North America (Allianz) and distributed by its affiliate, Allianz Life Financial Services, LLC, member FINRA. 5701 Golden Hills Drive, Minneapolis, MN 55416-1297. 800.542.9127 www.allianzlife.com

This content does not apply in the State Of New York.

Product and feature availability may vary by state and broker/dealer.

IASI-102 3/2026

(L4053-01)

[End of on-screen disclosures]

A solution built for your clients’ goals

With Index Advantage+ Select Income™ with the Lifetime Income Benefit Rider II,2 you now have the freedom to select WHEN to start lifetime income and WHAT strategies best match your clients’ income needs.

Flexibility to start income anytime

Whether you can wait and continue to grow your income potential, or you need income sooner, you have the flexibility to start your income when it makes sense for you. Income payments can begin any time after one index year and as early as age 50.

*Your Income Benefit Date cannot begin within 14 calendar days before an Index Anniversary.

Two options to receive income

When your client chooses to start receiving income, the amount they receive is determined by their current contract value and one of two income payment options to suit their income needs. With Index Advantage+ Select Income™, they can choose:

Level Income

Consistent, dependable income for life.

Level Income offers the reassurance of predictable payments, so they know exactly what their minimum income payment will be for the rest of their life.3

Level Income may be appropriate if they want:

- Income payments that will start higher and be predictable, because they should never decrease.3,4

- Higher income early in their retirement, when they’re likely to be more active or have higher immediate expenses.

Dynamic Income

Gives an opportunity for payment increases.

Dynamic Income offers a change in the income payment amount (positive or negative) each Index Anniversary based on the performance of their selected index options.5

Dynamic Income may be appropriate if they want:

- Income payments that start out lower but have the potential to change over their lifetime based on index option performance (positive or negative).5

- The potential for payments to increase can help address the effects of inflation over a long retirement, and the opportunity for more income over a lifetime.

Regardless of the income option they choose, they will have the flexibility to allocate to any available 1-year term index option when they elect income payments.6 Keep in mind, they could experience different outcomes based on their selected index option(s) and index performance. To learn more about your available index options, see the Index Options Guide (PDF).

Harness the power of Dynamic Income

With the Dynamic Income option, you can find a 1-year strategy that aligns with your clients’ risk tolerance and financial goals, whether that’s aggressive, conservative, or somewhere in between.

Risk and return potential spectrum

Diversifying index option allocations within a RILA does not ensure a positive performance credit in any term.

Resources to learn more

Selecting income strategies – in action

Meet Mary, a hypothetical 65-year-old client.

Objective: Mary is planning to choose multiple index strategies over the course of her retirement income years, based on changes in her risk tolerance.

Meet John, a hypothetical 70-yr-old client.

Objective: John appreciates the flexibility of being able to choose multiple index options, but he is planning to choose one index strategy and maintain it throughout retirement.

The characters are fictional and do not represent actual Allianz® clients or experiences. Your clients should consider the product’s features and benefits and consult with you regarding their investment objectives and risk tolerance before purchasing this product and allocating to one or more of the index strategies.

Ready to experience a reimagined income RILA?

For details and support, call our Sales Desk today at 800.542.5427.

1 Allianz Center for the Future of Retirement® conducted the 4Q 2025 Quarterly Market Perceptions Study in November 2025 with a nationally representative sample of 1,005 respondents age 18+. The Allianz Center for the Future of Retirement® produces insights and research as a part of Allianz Life Insurance Company of North America.

2 The Income Benefit is automatically included in the contract at issue for an additional rider fee of 0.70% that is accrued daily and deducted on each quarterly contract anniversary, calculated as a percentage of the charge base, which is the contract value on the preceding quarterly contract anniversary, adjusted for subsequent purchase payments and withdrawals.

3 Assumes all terms of the contract are followed. Once established, the annual maximum income payment can only decrease if you take an excess withdrawal. Excess withdrawals reduce your contract value, income payments, and any guaranteed death benefit value, and may end your contract.

4 It is possible for annual maximum income payments with Level Income to increase from one income benefit anniversary to the next. See prospectus for full details.

5 Payment increases or decreases are based on the weighted average of the performance credits and any locked index option values. While Dynamic Income provides the potential for greater annual income payments if there is positive index option performance, negative index option performance may significantly reduce the annual maximum income payment if you allocate to the Index Dual Precision Strategy, Index Precision Strategy, Index Guard Strategy, or Index Performance Strategy index options.

6 Both 1-year term and multi-year term index options are available during accumulation, prior to electing income.

Income payments can begin anytime up to 14 calendar days before an Index Anniversary once you reach age 50 and have satisfied the 1-index-year income payment waiting period.

RILAs provide indexed return potential with the opportunity for varying levels of protection through multiple index options available prior to receiving annuity payments, tax-deferred growth potential, a variety of annuity options, and a death benefit during the accumulation phase.

RILAs are subject to investment risk, including possible loss of principal. Investment returns and principal value will fluctuate with market conditions so that contract value, upon distribution, may be worth more or less than the original cost.

For more complete information about Index Advantage+ Select Income™ and any available variable option(s), call Allianz Life Financial Services, LLC at 800.542.5427 for a prospectus. The prospectuses contain details on investment objectives, risks, fees, and expenses, as well as other information about the RILA, index options, and any available variable option(s), which your clients should carefully consider. Encourage your clients to read the prospectuses thoroughly before sending money.

Withdrawals will reduce contract values (including any Cash Value) and the value of any potential protection benefits. Withdrawals taken within the period stated in the prospectus will be subject to a withdrawal charge or a Market Value Adjustment (MVA), depending on the product. All withdrawals are subject to ordinary income tax and, if taken prior to age 59½, may be subject to a 10% federal additional tax.

Guarantees are backed solely by the financial strength and claims-paying ability of the issuing insurance company. Variable annuity guarantees do not apply to the performance of the variable subaccount(s), which will fluctuate with market conditions.

Products are issued by Allianz Life Insurance Company of North America and distributed by its affiliate, Allianz Life Financial Services, LLC, member FINRA, 5701 Golden Hills Drive, Minneapolis, MN 55416-1297. 800.542.5427 www.allianzlife.com (L40538-01)

This content does not apply in the state of New York.

For broker/dealer use only – not for use with the public.